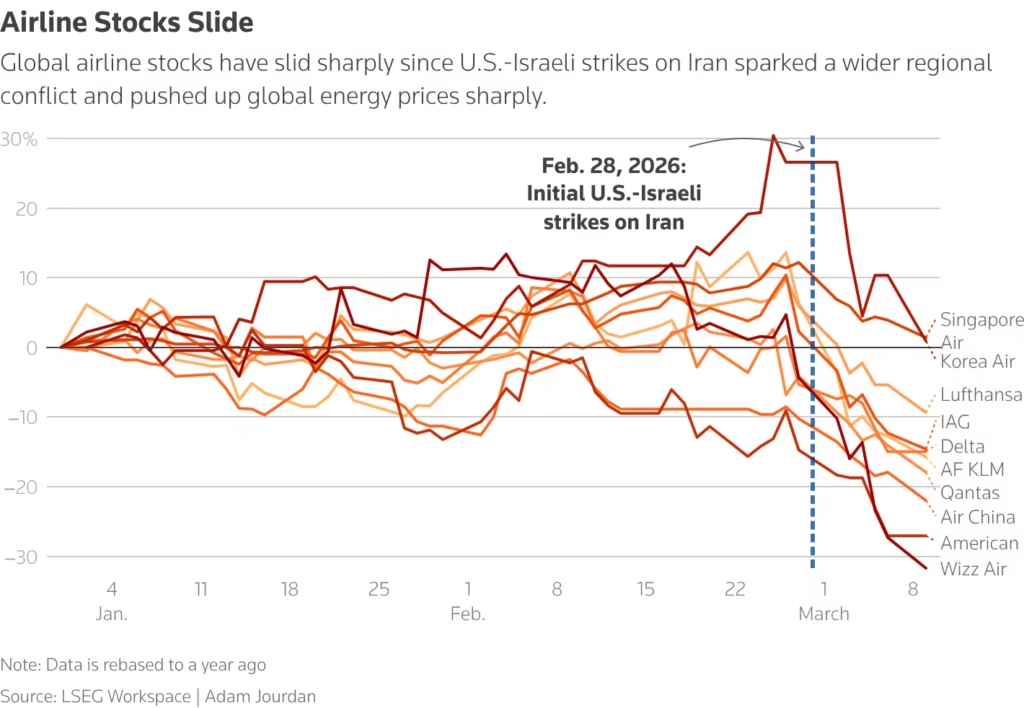

US and European airline stocks experienced a sharp contraction this week as global crude oil prices surged past the $100 per barrel mark.

This pricing shift introduces immediate volatility into the aviation sector, where fuel typically represents 25% to 35% of total operating expenses. Market participants are reacting to the increased risk of margin erosion as carriers struggle to pass these costs onto consumers through fare adjustments.

The current price action mirrors historical periods of energy instability, such as the 2008 financial crisis and the 2022 geopolitical shifts. However, the present environment is complicated by post-pandemic debt loads and ongoing labor negotiations.

Unlike previous cycles, airlines are operating with limited capacity buffers and a heightened sensitivity to input cost fluctuations. This sensitivity is particularly acute for carriers with unhedged fuel portfolios.

- Brent Crude Spot: $102.45 per barrel (+6.8% WoW)

- NYSE Arca Airline Index (XAL): -5.2% session decline

- Jet-A1 Crack Spread: +$12.50 above crude baseline

- Average Fuel Burn Cost: Increased by $0.18 per available seat mile (ASM)

- Year-to-Date Fuel Expenditure Variance: +14.2% against Q1 projections

The immediate correlation between Brent Crude spikes and equity sell-offs underscores the fragility of current recovery trajectories. While demand for long-haul travel remains robust, the cost of servicing that demand has escalated beyond the break-even points established in annual budgets.

Analysts observe that for every $10 increase in the price of oil, the industry’s collective bottom line suffers a multi-billion dollar impact. As market participants digest the latest Airline News, the focus shifts to how individual carriers manage their hedging derivatives to mitigate these spot price shocks.

In the United States, major legacy carriers like Delta Air Lines and United Airlines saw shares drop between 4% and 6% in midday trading. These entities have largely moved away from aggressive fuel hedging in recent years, preferring to rely on operational efficiency and refinery ownership.

The strategy of owning refining capacity, as seen with Delta’s Trainer refinery, provides a partial buffer but does not fully insulate the parent company from crude price spikes. This exposure forces a direct trade-off between fleet modernization and short-term liquidity maintenance.

European carriers, including Lufthansa Group and IAG, face a double-edged sword: rising fuel costs and a weakening Euro against the US Dollar. Since jet fuel is priced globally in USD, European operators are paying a premium twice—once for the commodity and once for the currency conversion.

This fiscal pressure is compounded by the European Union’s Emissions Trading System (ETS) costs, which are also tethered to energy production metrics. The resulting squeeze on discretionary cash flow threatens to stall ambitious carbon-neutrality initiatives scheduled for the 2030 window.

From an operational standpoint, high fuel prices often lead to the premature retirement of inefficient airframes. Carriers operating older Boeing 767 or Airbus A340 fleets are finding these assets increasingly toxic to their balance sheets.

The shift toward the Airbus A321neo and Boeing 737 MAX becomes a necessity rather than a preference. However, supply chain delays at major OEMs mean that many airlines are forced to continue flying less efficient ‘gas-guzzlers,’ further exacerbating the impact of $100+ oil.

Safety protocols also come under the watchdog lens during periods of financial duress. While regulatory compliance is non-negotiable, the secondary effects of cost-cutting can manifest in deferred non-essential maintenance or reduced pilot training overhead.

Senior dispatchers warn that financial pressure must not translate into operational shortcuts. Historical data suggests that periods of extreme fiscal stress require heightened oversight from the FAA and EASA to ensure that safety margins remain absolute despite the shrinking profitability of every flight hour.

Furthermore, the surge in crude prices complicates the adoption of Sustainable Aviation Fuel (SAF). Currently, SAF is significantly more expensive than traditional Jet-A1. When the baseline price of fossil-derived fuel rises, the price of SAF often follows suit due to shared feedstock and logistics costs.

This price parity gap remains a significant hurdle for the industry’s green transition, as airlines are less likely to invest in expensive alternatives when their primary fuel bill is already at record highs.

The regulatory landscape is also shifting in response to these economic pressures. Some jurisdictions are considering temporary relief on fuel taxes, though such measures are often politically unpopular given current environmental targets.

The aviation industry finds itself caught between the mandate to decarbonise and the immediate need to survive a high-inflation energy market. This tension is likely to lead to further consolidation within the sector as smaller, less capitalized regional carriers become targets for acquisition or face insolvency.

Investors are now scrutinising the ‘revenue per available seat mile’ (RASM) versus ‘cost per available seat mile’ (CASM) metrics with renewed intensity. If CASM continues to rise due to fuel, and RASM cannot keep pace because of consumer price sensitivity, the airline sector may enter a period of prolonged stagnation.

In conclusion, the breach of the $100 per barrel mark represents a significant stress test for the global aviation industry. The ability of carriers to navigate this period depends on their hedging maturity, fleet age, and the robustness of their route networks. Watchdog agencies must remain vigilant to ensure that fiscal austerity does not compromise the high safety standards that define modern commercial flight. The coming months will determine which carriers have the structural integrity to withstand this energy shock and which will be forced into radical restructuring.

For additional operational briefings and the latest Airline News, monitor our dedicated aviation intelligence category.

FAQ

Q1. Why do rising oil prices affect airlines?

Fuel is one of the largest operating expenses for airlines, often accounting for 25–35% of total costs, so oil price increases significantly impact profitability.

Q2. What happens to airline stocks when oil prices rise?

Airline stocks typically decline because higher fuel costs reduce profit margins and increase operational risk.

Q3. How do airlines manage fuel price volatility?

Airlines often use fuel hedging strategies, fleet modernization, and route optimization to mitigate the financial impact of rising oil prices.

Q4. What is CASM and RASM in aviation economics?

CASM (Cost per Available Seat Mile) measures operating cost efficiency, while RASM (Revenue per Available Seat Mile) measures revenue generation per seat mile.

Q5. Why is jet fuel tied to crude oil prices?

Jet fuel is refined from crude oil, so its price closely follows global crude oil market fluctuations.